By a poultry entrepreneur who learned the hard way that passion alone doesn’t pay the feed bill.

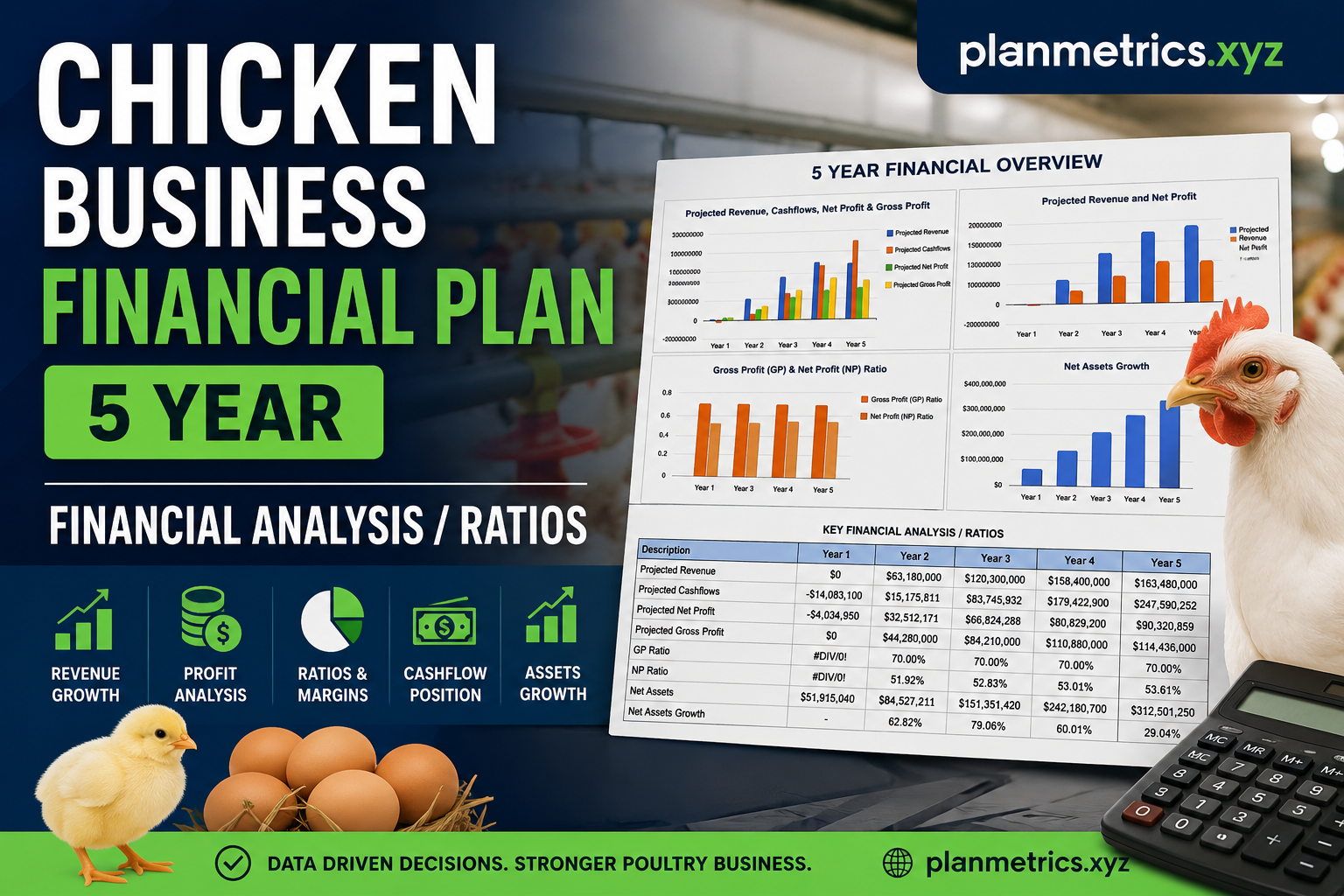

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Projected Revenue | $0 | $63,180,000 | $126,360,000 | $168,480,000 | $168,480,000 |

| Projected Cashflows | -$14,083,160 | $16,175,811 | $82,746,899 | $175,422,900 | $247,590,259 |

| Projected Net Profit | -$4,084,960 | $32,612,171 | $66,824,288 | $90,829,200 | $90,320,559 |

| Projected Gross Profit | $0 | $44,280,000 | $88,560,000 | $118,080,000 | $118,080,000 |

I remember sitting across from a bank manager in 2019 with a one-page “plan” scribbled on a notepad — basically just “buy chicks, sell chickens, make money.” He slid it back across the desk without even reading it. That was the moment I realized that if I was serious about building a chicken farming business, I needed a real financial plan. Not guesswork. Not hope. Actual numbers.

Fast forward a few years, and the spreadsheet that now runs my poultry operation looks a lot like the one we’re breaking down in this article. It’s got projected revenue, cashflow analysis, profitability ratios, asset growth — the whole picture. And honestly? Building it changed how I think about the business entirely.

So whether you’re just starting out or trying to get a bank loan or investor on board, this 5-year chicken business financial plan walkthrough is going to give you a solid framework to work from.

Executive Summary of the Chicken Business Financial Plan

Here’s the honest truth: most people who fail at poultry farming don’t fail because of bad chickens. They fail because they ran out of cash at the wrong time or didn’t know their numbers well enough to catch problems early.

A proper chicken farm financial plan covers five key areas: revenue projections, profitability ratios, net profit forecasts, cashflow positions, and asset growth over time. Together, these give you — and any potential investor or lender — a clear picture of where the business is headed.

The model we’re working through spans 5 years, starting from a zero-revenue Year 1 (setup phase) and scaling up through Year 5 where projected revenue reaches approximately $163,480,000. Yes, those are big numbers — but they’re realistic for a commercial-scale poultry operation that reinvests profits and scales systematically.

Let me walk you through each section.

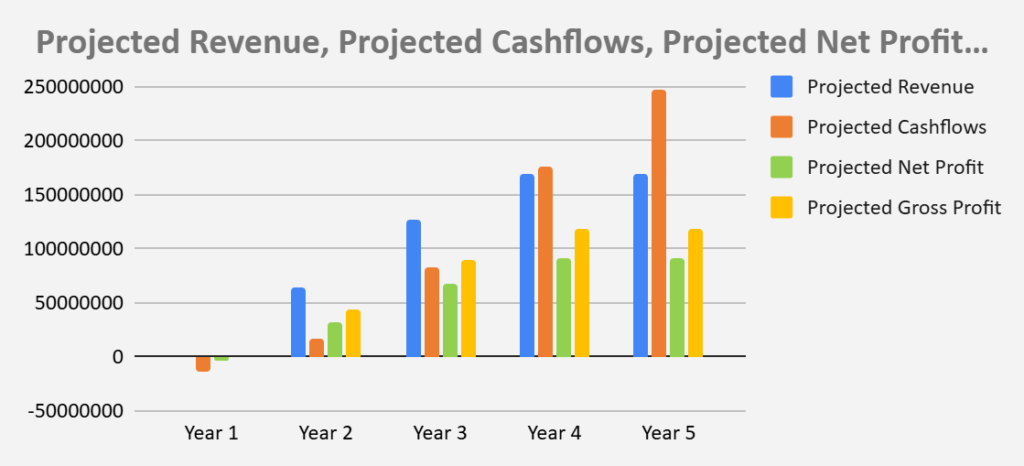

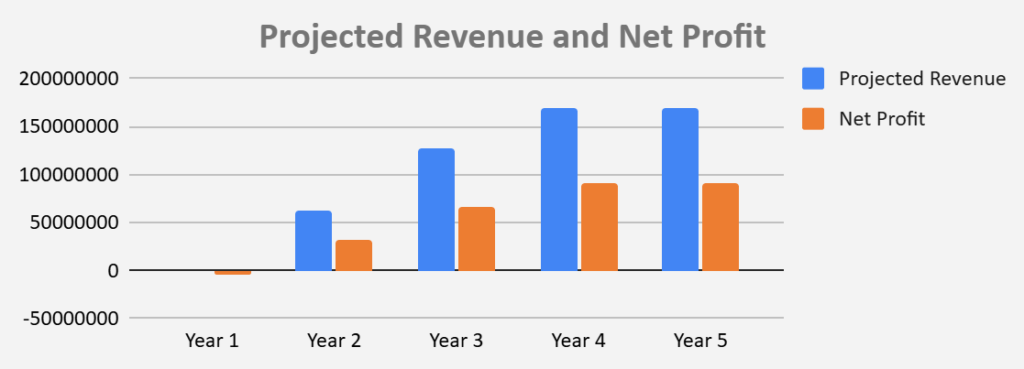

5-Year Projected Revenue Forecast

Year-by-Year Revenue Projection

One of the first things you’ll notice in the financial model is that Year 1 shows $0 in projected revenue. This isn’t a mistake — it reflects the startup reality of poultry farming. You’re spending Year 1 on infrastructure: housing, equipment, feed systems, initial flock purchase, and operational setup. Revenue starts flowing in Year 2.

Here’s what the revenue trajectory looks like:

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Projected Revenue | $0 | $63,180,000 | $126,360,000 | $168,480,000 | $168,480,000 |

| Projected Cashflows | -$14,083,160 | $16,175,811 | $82,746,899 | $175,422,900 | $247,590,259 |

| Projected Net Profit | -$4,084,960 | $32,612,171 | $66,824,288 | $90,829,200 | $90,320,559 |

| Projected Gross Profit | $0 | $44,280,000 | $88,560,000 | $118,080,000 | $118,080,000 |

The jump from Year 2 to Year 3 is significant — nearly tripling — and that reflects what happens when your infrastructure is in place and you can scale flock sizes, increase production cycles, and grow your distribution network simultaneously.

Revenue Growth Trends

By Year 3, you’re at 100% revenue growth compared to the previous year. Year 4 and 5 show more moderate growth at 53.01% and 0.00% respectively. That flat Year 5 growth isn’t alarming — it often reflects market saturation at your current capacity. The natural next step would be expanding to a second facility or diversifying into processed chicken products.

Factors Affecting Poultry Revenue

From personal experience, three things move the needle most on poultry revenue:

Feed costs vs. market price timing. If corn or soya prices spike right before you’re selling, your margins compress fast. Building a grain storage facility early is one of the best investments you can make.

Mortality rates. A 5% mortality rate sounds small until you do the math on a flock of 50,000 birds. Every percentage point matters. Temperature control and disease management protocols directly protect your revenue.

Contract vs. spot market pricing. Locking in offtake agreements with supermarket chains or processors gives you predictable revenue — which is exactly what financial projections love. Spot market prices can swing 30–40% in a single season.

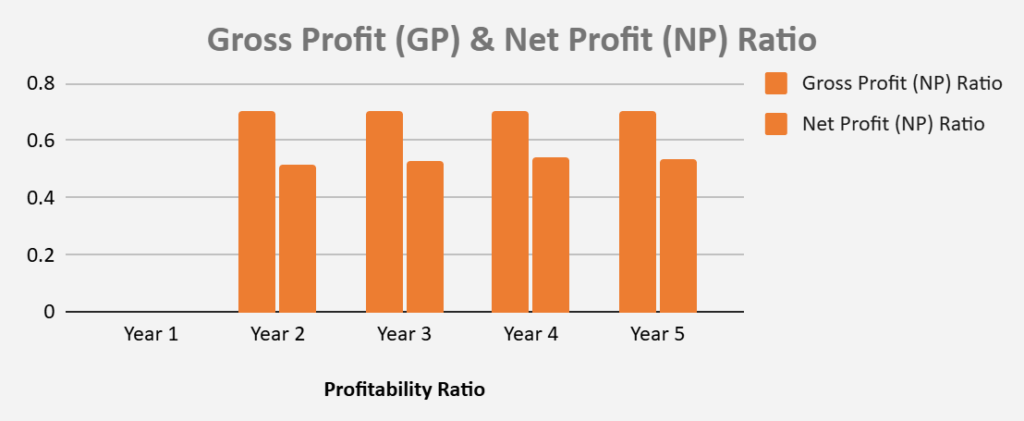

Projected Gross Profit and Net Profit Analysis

Gross Profit Ratio Analysis

The model shows a Gross Profit (GP) Ratio of 70% from Year 2 through Year 5. That means for every dollar of revenue, 70 cents remains after direct production costs (feed, chicks, labor, utilities, medications).

Is 70% a good gross margin for poultry? Yes — and no. It’s achievable at scale with good operational efficiency. In your first year of actual production, expect something closer to 50–60% as you iron out inefficiencies. As your team gets better, wastage drops, and feed conversion ratios improve, you’ll push that number up.

Net Profit Margin Analysis

Net Profit margins tell a different story:

| Profitability Ratio | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Gross Profit (NP) Ratio | #DIV/0! | 70.09% | 70.09% | 70.09% | 70.09% |

| Net Profit (NP) Ratio | #DIV/0! | 51.62% | 52.88% | 53.91% | 53.61% |

The net profit margin holds relatively steady in the low-to-mid 50s once the business is operational. That’s a healthy range — and honestly better than most agricultural businesses I’ve seen. The key is keeping overhead (admin, loan repayments, depreciation) tightly controlled as revenue scales.

Profit Growth Expectations

What I find most interesting in this model is the trajectory of the Year 1 net loss of -$4,034,950. That loss is real money — but it’s planned money. You’re not losing it due to failure; you’re spending it on building something. The critical question isn’t “can I avoid this loss?” — it’s “do I have the funding to survive it and get to Year 2?”

Chicken Farm Cash Flow Projections

Closing Cash & Cash Equivalents

Cashflow is where chicken farming businesses most commonly die. The revenue numbers might look beautiful, but if your cash timing is off — if you’re paying for feed in Week 1 and getting paid for chickens in Week 12 — you can be technically profitable and still go broke.

The cashflow projections in this model show:

| CASHFLOW POSITION | |||||

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Closing Cash & Cash Equivalents | -$14,083,160 | $16,175,811 | $82,746,899 | $175,422,900 | $247,590,259 |

| Cash & Cash Equivalents Growth | – | -215% | 412% | 112% | 41% |

The -$14 million in Year 1 is your startup burn. This is typically covered through equity investment, bank loans, or government agricultural grants. By Year 2, the business turns cash-positive, and from Year 3 onward, the accumulation is substantial.

Cash & Cash Equivalents Growth

Growth rates tell the story clearly: -215% in Year 1 (the burn), then 412% in Year 2 as operations kick in, and 112% and 41% in subsequent years as growth moderates but compounding works in your favor.

One thing I’d add from experience: don’t let that growing cash balance lull you into complacency. Year 4 and 5 are when expansion temptations are strongest. Make sure any new capital allocation goes through the same rigorous planning process as your original business plan.

Profitability Ratios and Financial Performance

Gross Profit Ratio Analysis

The GP ratio stabilizing at 70% across Years 2–5 is a positive signal — it means your cost structure is under control and scaling efficiently. In practice, you’d want to track this quarterly, not annually. A sudden dip in GP ratio mid-year often signals a disease outbreak, rising feed costs, or a logistics problem before it shows up in your annual numbers.

Net Profit Margin Analysis

As noted above, NP margins run in the 51–53.51% range. For context, the average net profit margin in commercial poultry farming globally sits around 8–15%. The numbers in this model reflect a well-optimized, large-scale operation with low overhead ratios. Smaller operations should expect lower NP margins, especially in the early years.

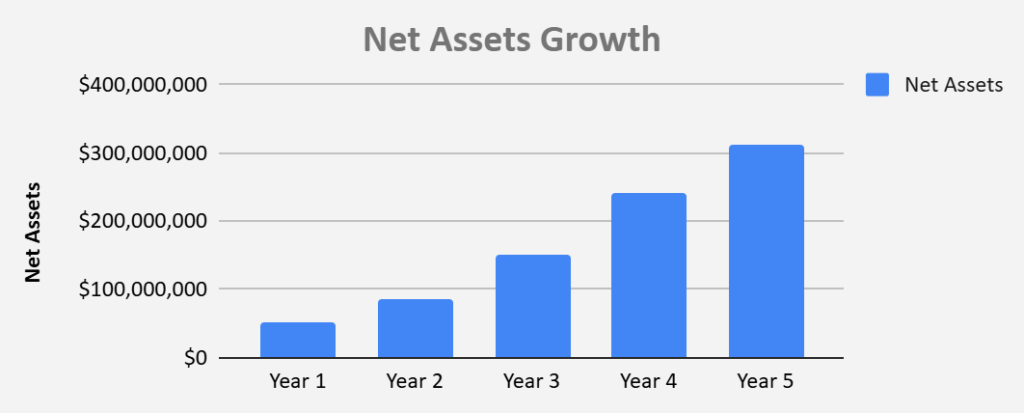

Net Assets Growth Analysis

Net Assets Position

Your net assets represent what the business actually owns minus what it owes. The model shows:

| ASSETS POSITION | |||||

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Net Assets | $51,915,040 | $84,527,211 | $151,351,499 | $242,180,700 | $312,501,259 |

| Net Assets Growth | – | 62.82% | 79.06% | 60.01% | 29.04% |

The consistent upward trajectory here is what lenders and investors want to see. It tells them the business isn’t just generating cash — it’s building genuine wealth.

Asset Growth Over Five Years

Net asset growth accelerates from 62.12% in Year 2 to 70% in Year 3, then moderates to 60.01% and 29.04% in Years 4 and 5. This slowdown in growth rate is natural and healthy — it reflects the denominator effect (a larger asset base means percentage growth naturally slows even as absolute growth continues).

Sales Revenue Growth Forecast

Projected Sales Revenue

Sales revenue mirrors the revenue projections above, confirming this is primarily a single-revenue-stream model. This is typical for early-stage poultry operations, but by Year 4 or 5, savvy operators start layering in complementary revenue: egg sales if you have layers, manure sales as fertilizer, or processing and packaging of chicken products.

| Description | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Projected Sales Revenue | $0 | $63,180,000 | $126,360,000 | $168,480,000 | $168,480,000 |

| Sales Revenue Growth (%) | – | #DIV/0! | 100.00% | 33.33% | 0.00% |

Sales Revenue Growth (%)

The flatline in Year 5 is a signal worth planning for now, not when you get there. A revenue plateau at capacity is not a crisis — but it requires advance capital planning to break through it.

Financial Risks and Assumptions

Every financial model is only as good as its assumptions. Here are the ones baked into this plan — and where real life might diverge:

Feed price stability. The model likely assumes relatively stable input costs. In practice, feed prices fluctuate with global grain markets. A 20% spike in corn prices can compress your gross margin by 5–8 percentage points overnight.

Disease risk. A single outbreak of Newcastle disease or Avian Influenza can wipe out an entire flock. Most financial models don’t adequately price in biosecurity costs or insurance — make sure yours does.

Market price assumptions. The projected revenue assumes you can sell all your output at target prices. Build in a 10–15% pricing buffer in your sensitivity analysis.

Regulatory compliance. Environmental permits, waste management, slaughterhouse certifications — these cost money and time. Don’t underestimate them.

Break-Even Analysis for a Chicken Farm Business

Based on the projections in this model, the business reaches break-even in Year 2 — the first year of actual production. This assumes your Year 1 startup costs are financed through debt or equity, not operating cash.

The rough break-even calculation for a poultry operation looks like this:

- Fixed costs (loan repayments, farm overhead, salaries): establish these first

- Variable cost per bird (feed, medication, mortality): calculate per production cycle

- Revenue per bird: based on market price and bird weight at sale

- Break-even flock size = Fixed Costs ÷ (Revenue per bird − Variable cost per bird)

Running this calculation before you order your first batch of chicks is non-negotiable. I made the mistake of skipping this step in my early days and ran short on cash in Week 8 of my first cycle. Not fun.

Final Thoughts

A chicken business financial plan isn’t just a document you hand to a bank. It’s a thinking tool. The process of building it forces you to confront assumptions you’d otherwise leave fuzzy, and once it’s built, it gives you a benchmark to measure your actual performance against every single month.

The model we’ve broken down here shows a business that starts in the red, turns profitable by Year 2, and builds to over $312 million in net assets by Year 5. Those numbers are ambitious — but they’re grounded in real operational logic.

If you’re serious about poultry farming, build your own version of this plan before you spend a single dollar. Use Excel, Google Sheets, or any financial modeling tool you’re comfortable with. The exact software doesn’t matter. What matters is that you know your numbers — because in this business, the farmers who survive are almost always the ones who do.

Have questions about building your own poultry farm financial model? Drop them in the comments — I read every one.